Student housing still has demand, but developers need a sharper strategy than before.

The right markets remain strong, and well-located projects can still outperform.

But developers need to evaluate rent growth, preleasing, supply, on-campus demand, and product fit before design begins.

Student housing only pencils out when market and design strategy align early.

Rent Growth Can No Longer Carry the Deal

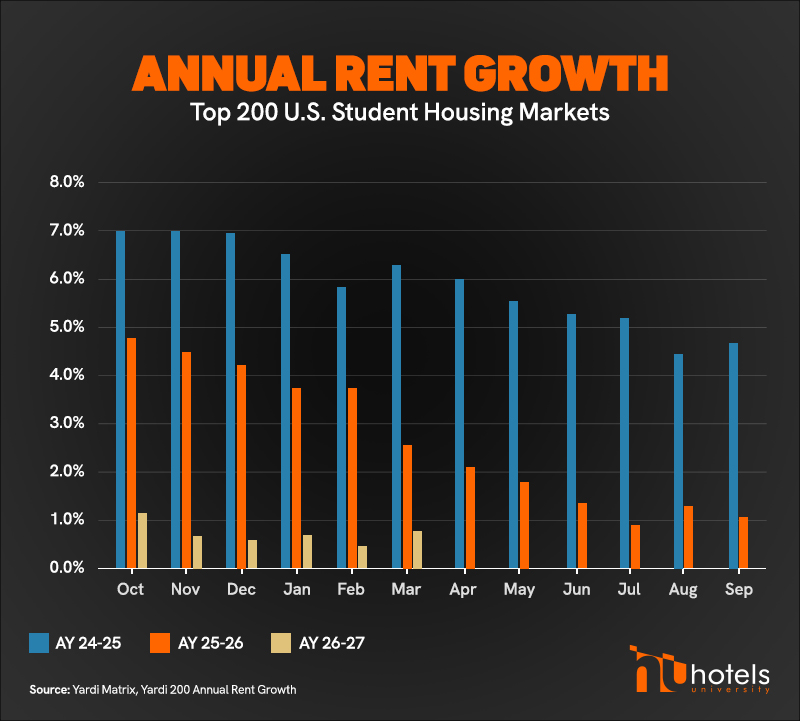

- According to Yardi, average rent growth across the Yardi 200 slowed to 0.8% year-over-year in March 2026, well below 2.6% in March 2025 and 6.3% in March 2024.

- Preleasing is ahead nationally, but markets like Purdue, Arkansas, UCF, NC State, and the University of Tennessee are trailing. New supply is a major reason.

Deals need to work at today’s rents. That math starts in planning.

Enrollment Headlines Can Be Misleading

Enrollment growth matters, but it does not guarantee strong lease-up, rent growth, or the right unit mix.

Online enrollment can grow while physical attendance stays flat.

Housing demand follows students on campus, not headcount on a report.

In secondary and tertiary markets, especially, verify on-campus demand before treating the numbers as a green light.

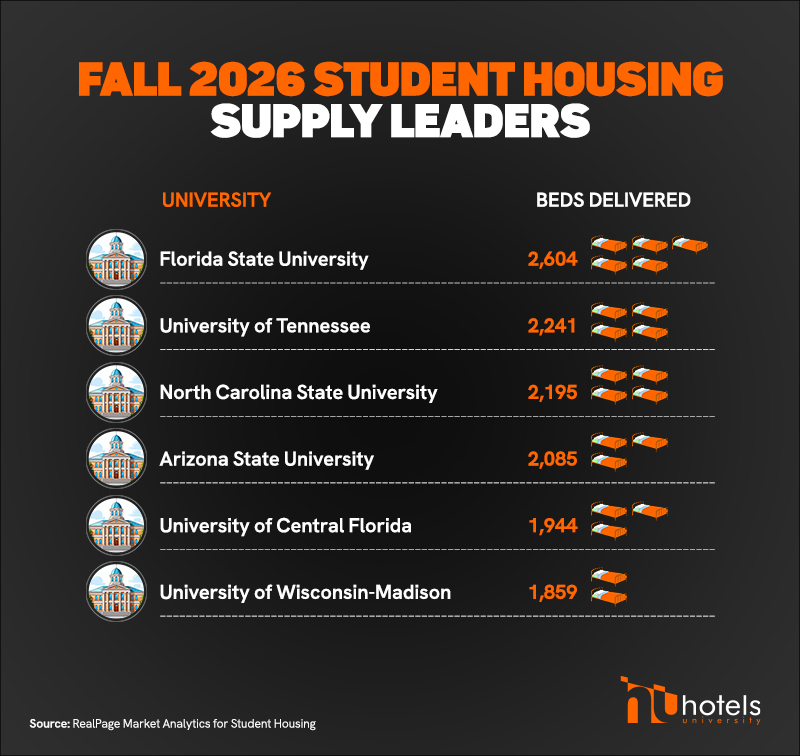

Strong Schools Can Still Be Oversupplied

A strong university does not mean a strong market.

Florida State alone is delivering over 2,600 beds this fall. Tennessee, NC State, and Arizona State each top 2,000.

When that much supply lands at once, lease-up slows and concessions rise.

Where Student Housing Still Pencils

- The best markets share one trait: on-site enrollment is growing faster than new supply. Ole Miss, Auburn, UT San Antonio, Texas State, Kennesaw State, LSU, and San Jose State stand out.

- Location still matters. Beds within a quarter mile of campus command the highest rents, while mid-rise and high-rise projects are leading preleasing.

- Farther sites can still work, but only with tighter layouts, lower costs, and a clear reason for students to choose them.

The Next Cycle Will Be Won in Planning

Even a strong student housing deal can miss if the product, timing, and assumptions are not aligned from the start.

BASE4 helps developers test the deal early with:

- Cost-aware design tested against real pro formas

- Unit mix and amenity load calibrated to today’s rents

- Prefab and offsite expertise for faster, cheaper delivery

- In-house architecture, structural, MEP, and interiors

- 100% Revit coordination to reduce field errors and delays

- Early planning before weak assumptions get locked in

Thank you,

Blair Hildahl

Blair@hotelsuniversity.com

608.304.5228